Drawdowns, AFT, ACH, 3rd party e-wallets and card acquisition.

All the methods of funding your user's wallet dissected.

People have voted about the next topic for discussion in my last article about ISO standards and I agreed. Today we’ll talk about funding user’s accounts: AFT, Reverse-Wires, standard ACH and cards (broader than AFT).

Before I go any further here, I have to mention that I have moved to a role of Enterprise Account Executive at Moov.io - a payment processor. Anything found in my content is just my opinion and doesn’t represent the company I work for.

My opinions will, no doubt, continue to be mildly biased just like they were when I worked at Checkbook. I keep the bias to a true minimum (see the sources I site in my articles) but it’s only fair to warn you.

Account funding methods

Today there are 5 main methods that you can use to fund your user’s wallets:

AFT - Account Funding Transactions

Drawdowns (Reverse Wires)

ACH

PayPal, Venmo, CashApp and other 3rd party P2P wallets

Debit and credit card acquisition

Each one has its own pros and cons in a wide variety of forms so we’ll dive into each one and break them down. Each one has dozens of pros and cons so I’ll only focus on those that I consider to be “major”.

Quick definition before we proceed, for the purpose of this article, I define Wallets as a 3rd party-offered tool that allows users to store funds online for more flexible spending. Think of your balance in your brokerage platform or PayPal as a wallet.

1. Account Funding Transactions.

One of the most extensive articles that I have written so far, you can read it here:

In short, AFT allows you to instantly pull funds from a connected debit card into a user’s wallet. The funds will be made available to you (and therefore to your user), almost instantly. Pros and cons of AFT:

Pros:

Much faster than any alternative pull (exception is RFP) with settlement delay of roughly 5 minutes. This number depends on the provider but with Moov.io, the delay is less than 5 minutes.

You can find an example of how hundreds of banks use this solution to allow their customers to instantly fund their accounts through Rapid Transfers.Significantly reduced reversal period. The payment can be reversed by the sender only while it is settling which takes 1 business day. Don’t confuse settlement with fund availability.

Fund availability = funds are made available to you by your payment processor. The processor takes a risk on such funds which is why AFT isn’t available for “high risk” industries.

Settlement = the funds actually settle into the bank account where the pull was initiated.Cheaper than standard debit rails. Debit rails come at about 1-2% (very rough averaged numbers) while AFT is sitting closer to a fixed 1%.

Cons:

Limited use-case support. Here is the full list of supported and prohibited use-cases.

Limited coverage: covering only Visa and Mastercard issued debit cards.

Much more expensive than standard ACH pulls. This solution is only viable for those who value decreased settlement delay over costs.

Limited availability. This rail has been introduced very recently (by the metrics of financial systems) and isn’t widely available. Checkbook.io is amongst the few PSPs that offer AFT

Summary: great rail suitable for the vast majority of Me to Me (account funding) transfers. But AFT is not to be confused with a universal workaround for standard debit and credit card processing.

2. Drawdowns (Reverse Wires).

Drawdowns (aka Reverse Wires) are exactly what the name suggests: wires that can be “pulled” from client’s connected bank account. The formal definition that I liked comes from NatPay and defines it as follows: “…account holder authorizes another party, such as a vendor, to withdraw funds from their account via a wire transfer.”

This rail requires a more sophisticated connectivity than standard ACH debits. Each bank has its own set of requirements to enable reverse wires but generally it requires your customer to reach out to their bank and ask for a drawdown enablement form. The form gets completed by the customer and sent to the bank (sometimes hard copy is required) and only then can it be enabled.

There might be additional steps required by your payment processor. Pros and cons of Drawdowns (Reverse Wires):

Pros:

Speed and simplicity once setup: near instant funding of accounts that doesn’t require your client to log into their bank account and initiate the wire. That covers pretty much all the perks.

Cons:

Setup complexities: there is no universal drawdown enablement schema (hence I don’t have the article on the subject matter). It heavily depends on the payment provider you use and the recipient bank and always requires manual work.

Setup time: because of the complexities mentioned in the point prior, the setup time may vary drastically but usually takes ~2 weeks, making this solution only suitable for Mid-Market/Enterprise B2B transactions.

Limited coverage by banks: drawdowns are frequently not supported by the sender’s bank.

Cost: your customer is still paying for the wire but there might be additional setup fees and costs associated with the wire being a drawdown. Again, suitable only for large clients.

Summary: a great rail to introduce for your larger clients who need to be making somewhat frequent and large payments through your platform. Comes with a set of its own issue but very worthy for any client pushing $100,000+ per month to your accounts.

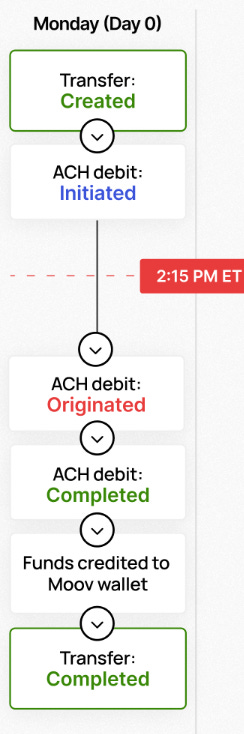

3. ACH

Good old ACH that we all are familiar with. I wrote a piece about Overnight and Same Day ACH and how to communicate the settlement schedules to your customers, you can read it here.

Important addition to the article I am referencing in the line above: there are faster settlement options such as “Faster same-day” ACH that removes the 2 day fund hold. The settlement schedule for it looks like this:

I don’t think I need to waste my breath further and we’ll go right into short pros and cons. Pros and cons of ACH:

Pros:

Coverage: Supported by every single American bank. No exceptions.

Cheap: the cheapest way of moving Fiat money electronically.

Supports large transactions: depending on your processing partner (like Moov (told you, there will be shameless plug ins like before)), you might be able to move $100,000,000 in a singular transaction (push or pull).

Cons:

Slow: in the 21st century the customer’s expectation is speed. ACH doesn’t offer it, having settlement delays of as long as 5 business days in many cases. Pull/push failures mentioned in the next point further contribute to the speed issue.

Prone to failure: on top of standard standard delays, the NSF (Not Sufficient Funds) and other R codes are a massive thorn in your side every time you try using ACH at scale.

Reconciliation issues: customizing the transaction descriptors for ACH transactions can be painful. This may result in your customers seeing random names on their banking statements and disputing perfectly valid transactions.

Summary: a great rail if you are valuing cost over speed and need to process large transactions. An absolute must-have as a backup option for almost any operation because of it’s 100% coverage of US banks.

4. PayPal, Venmo, CashApp and other 3rd party P2P wallets

Pals I don’t want to write. Sheer power of will here.

All of the above falls under the “Digital Wallet” (or e-wallet, depending on the generation you were born in) category. There are a lot of definitions for e-wallet, but for the purpose of this article, I’ll stick with e-wallet is a tool to store customer’s funds in a way that gives a customer additional perks not available through a bank.

Perks that are offered by e-wallets are countless: easier P2P payments, simplified UI, no maintenance fees etc. In what follows I’ll summarize pros and cons of using them as a funding source to fund other wallets - within your organization (presumably).

Pros:

Ease of use for the client: instead of connecting their bank account, they can just connect their e-wallet which is perceived by the client to be a safer action than connecting a bank account.

Extensive coverage: according to Pew Research, roughly 76% of Americans use one of the major e-wallets.

Instant funding: funds settle instantly in your account (depending on the integration you have with the funding wallet).

Cons:

Complex integration: being able to accept PayPal or Venmo as a pay-in method is a bit of a pain, especially if you integrate with them directly.

Risk: some e-wallets like CashApp are generally considered to be a “high risk” funding source because the origins of funds in the said wallets can be shady and the e-wallet doesn’t provide enough screening like banks do.

In my non-legal opinion, this is a very minor risk.Cost: depending on the agreement you have with the funding e-wallet organization like PayPal, such funding transactions might cost substantially more than alternative instant rails like RTP and FedNow.

Summary: a useful source of funding to have but not worth the hassle unless you have strong demand from your clients or if your payment provider can offer it out of the box.

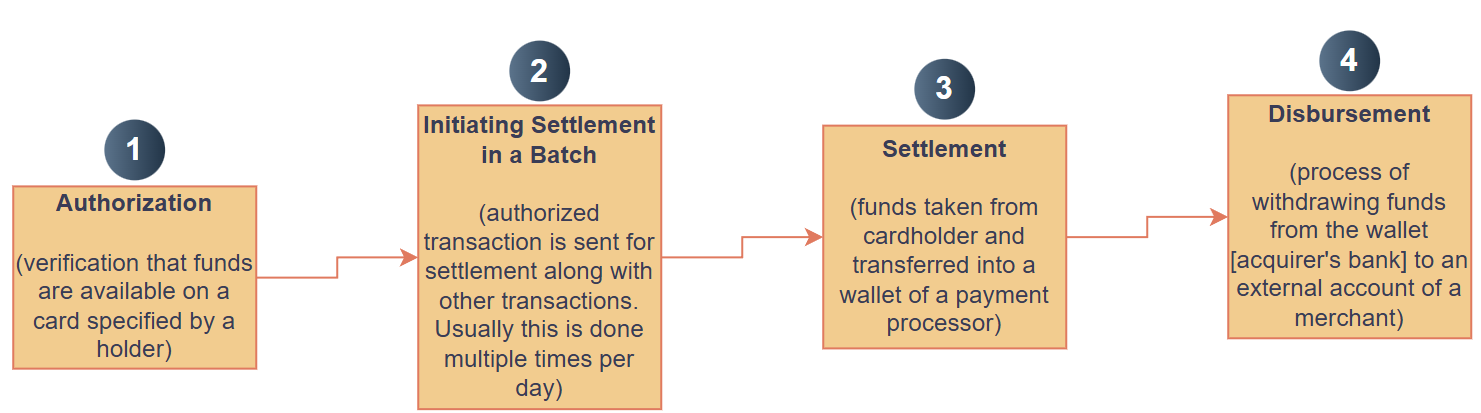

5. Debit and credit card acquisition*

There is a star * next to this “funding” method since it’s not conventional nor is it optimal for wallet funding.

The only way to use it as a way to fund a wallet is to issue an invoice to a client that then gets paid through standard debit/credit rails. Such a “funding” transaction wouldn’t be considered “funding”, but rather a bill pay transaction that happens to land into a wallet as an intermediary step.

Such a step is always present, whichever payment processor you may choose. Here is a diagram of simplified steps involved in card processing that results in Wallet funding:

Steps 1 and 2 are irrelevant to this specific article but I wanted to include them to draw a full picture.

Step 3 is where the funds are taken form the cardholder’s account and transferred into the acquirer’s account. From there, we move to step 4 where the beauty of storing funds in a Wallet really show. You are not limited to standard ACH into your bank account, instead you can push funds through Push to Card, RTP, Same Day ACH, PayPal, Venmo and other rails (depending on the provider).

That’s where modern PSPs (like Moov.io) really shine with the amount of rails offered as payout methods. But I digress, let’s get to the pros and cons of this method and wrap it up.

Pros:

Easy for the end-user.

Relatively fast. I have put “slow” in the next section and it is because things are relative and heavily depend on a multitude of factors. This method might be significantly faster than standard ACH pulls.

Cons:

Not really an account funding method. The wallet funding just happens to be a part of the card processing but again, it is technically not an account funding method.

Expensive. Depending on the industry you operate in, you might be paying 3%+ per transaction.

Might be slow. Depending on the processor you work with, the 2nd and the 4th steps might each take 2-3 business days (like it does with Stripe). More flexible and lean processors (again, like Moov), allow you to get access to your funds in total of ~1-2 days.

That’s a wrap. I am a bit tired so I’ll leave you with a simple call to action: check out my podcast AFT.finance where a lot of content similar to this is presented in a verbal format.

And of course, reach out to me if you need guidance in the payments space! Part of my role at Moov is to do just that at a charge of $0 so I’m happy to assist.